|

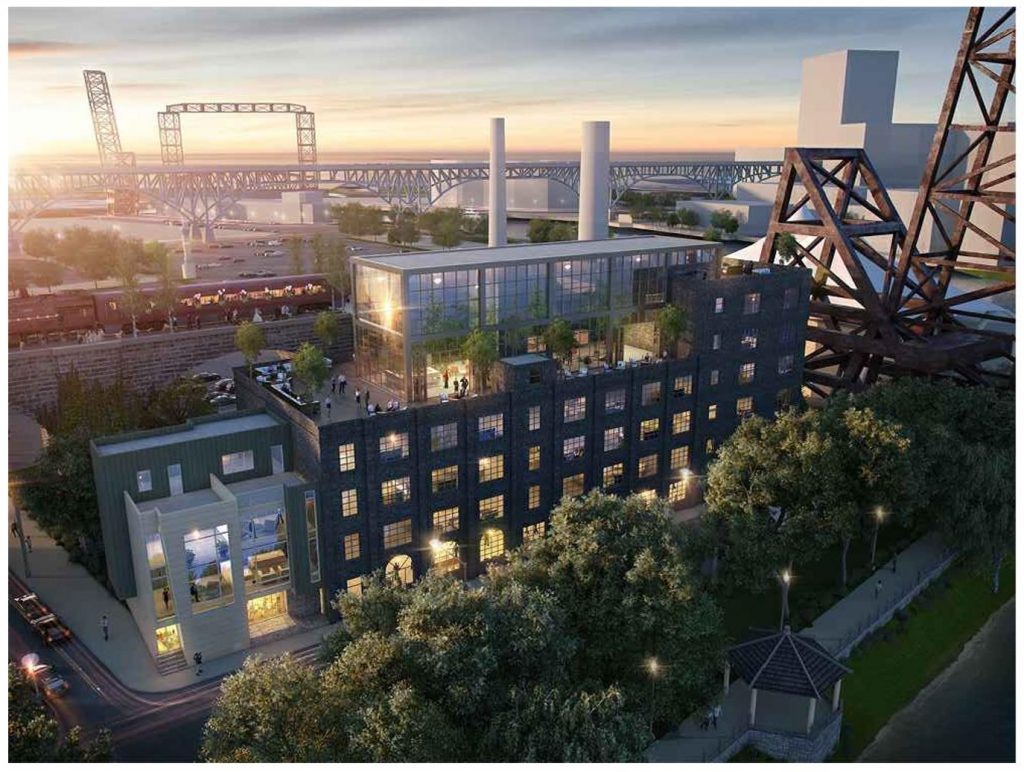

| A law firm hired by Stark Enterprises drafted the first Transfor- mational Mixed Use Development (TMUD) tax credit bill two years ago to aid its $350 million nuCLEus development planned in downtown Cleveland. A variant of that original bill could be moving closer to passage in Ohio’s General Assembly (Stark). CLICK IMAGES TO ENLARGE THEM |

The Ohio House of Representatives’ Economic and Workforce Development Committee today could accept major changes to a bill designed to create a Transformational Mixed Use Development (TMUD) tax credit to kick-start real estate mega-projects.

If accepted, the committee could take testimony on Substitute Senate Bill 39 at the following hearing, tentatively scheduled for Feb. 12 before moving the bill to the House floor for a vote by the 99-member legislative body.

As reported here last month, if the House passes the bill, it would set up a conference committee to iron out differences from an earlier version of the legislation that passed the Ohio Senate 32-1 last summer.

To offset the cost of “transformational” developments in Ohio, the proposed tax credit would refund to insurance companies up to 10 percent of their investment in TMUDs, as defined by the bill. State Sen. Kirk Schuring (R-29, Canton) is the bill’s primary sponsor. He submitted the latest proposed changes to the House committee.

Business and civic leaders throughout the state sought the tax credit because major developments in Ohio’s larger downtowns cost nearly as much to build as those in larger cities like New York and Chicago. However, Ohio developments command rents that are one-half to two-thirds less.

Thompson Hine LLP, drafted the first TMUD legislation two years ago at the request of Cleveland-based Stark Enterprises. It did so after Stark had tried and failed at producing other methods public-sector capital funding for its $350 million mixed-use nuCLEus development project in downtown Cleveland.

|

| Significant changes were made to the TMUD tax credit bill to benefit Ohio’s small towns that are bleeding jobs and younger residents to large cities in Ohio and elsewhere (State of Ohio). |

Another version of the same basic legislation unanimously passed the House in the previous legislative session in 2018 but that session expired before the Senate could pass it. The bill was re-introduced into the Senate in early 2019 at the start of the current two-year session.

More changes to the bill were desired this time around in order to garner more political support and move it out of committee to a vote in the full House, said Josh Ferdelman, legislative aide to State Rep. Paul Zeltwanger, chair of the House’s Workforce & Economic Development Committee.

Support for the bill was lagging among representatives of rural and small-town Ohio districts that have been losing jobs, opportunities and young people to larger cities during the so-called “Fifth Migration.”

In the past five years, Ohio’s largest metropolitan areas have been carrying the state’s economy, according to the U.S. Bureau of Labor Statistics. Ohio gained 227,000 jobs since the start of 2015. The metros of Cincinnati, Cleveland and Columbus accounted for 216,000 of those new jobs.

Adding in the next-largest metros of Akron, Dayton and Toledo, Ohio’s six largest urbanized areas gained 245,000 jobs. Without them, Ohio would have lost 18,000 jobs since 2015.

So new provisions to the TMUD bill are proposed to set aside 20 percent (or $20 million) of the tax credits available each year for projects in less populous areas. Specifically, the new provision specifies projects further than 10 miles from a major city that has a population larger than 100,000 people, according to an analysis and comparison of recently proposed versions of Sub. SB 39 by the Ohio Legislative Service Commission.

And in such areas, qualifying projects must have buildings only four stories in height with a total size of 75,000 square feet. The buildings do not have to be connected. That compares to 10 stories and 250,000 square feet for projects within 10 miles of a major city.

|

| This artist’s rendering of part of the massive bank lobby in the former Union Commerce Bank in downtown Cleveland belies its appearance today — an empty space waiting for an infusion of capital to bring it back to life as The Centennial. The TMUD tax credit could offer that infusion of capital (Millennia). |

The previous version of the bill considered TMUDs to be those whose new or to-be-renovated connected buildings are at least 15 stories tall, measure at least 350,000 square feet and contain any combination of retail, office, residential, recreation, structured parking or similar uses.

The new rural set-aside would replace a provision in the bill’s previous version that would increase the existing historic renovation tax credit percentage from 25 to 35 percent for projects in rural areas. Thus, certain small-town new-construction developments, not just small-town renovation projects, would qualify for tax credits.

Some other major proposed changes to the bill would terminate authority for approval of credits on June 30, 2022. Thus a new bill would have to be passed to continue the program into the next fiscal year. Administration and issuance of TMUD tax credits would be overseen by the Ohio Tax Credit Authority rather than the state’s Director of Development Services, as previously proposed.

Under the prior version of the bill, an awarded credit can equal 10 percent of documented development costs or, if the applicant is an insurance company contributing capital to the project, 10 percent of the capital contribution. That would remain, but the tax credit for any one project would be limited to $40 million.

While there would be no limit on the number of projects that may be certified as eligible for the tax credit, the total amount of tax credits would be limited to $100 million in each of fiscal year 2020 (which ends June 30, 2020), FY 2021 and FY 2022.

Unlike before, unused certifications would not carry over to later years. While projects would be ranked on their economic value and transformational impact, the ranking would be done separately for projects within 10 miles of a major city and those outside such a radius.

END

Thanks for keeping us up to date with new information about this important legislation!!